Depending on your firm’s distribution strategy, there are several ways to view the universe of data and invest your resources accordingly. One such approach is organising your data by product, assigning product ownership, and setting goals accordingly. Another emerging strategy is to take a client-centred approach which helps managers acknowledge the broader, long-term perspectives of their clients and tailor their allocation, client experience, and general distribution strategy using a data-driven approach.

Unlocking Long-Term Perspectives with CBOR Advantage

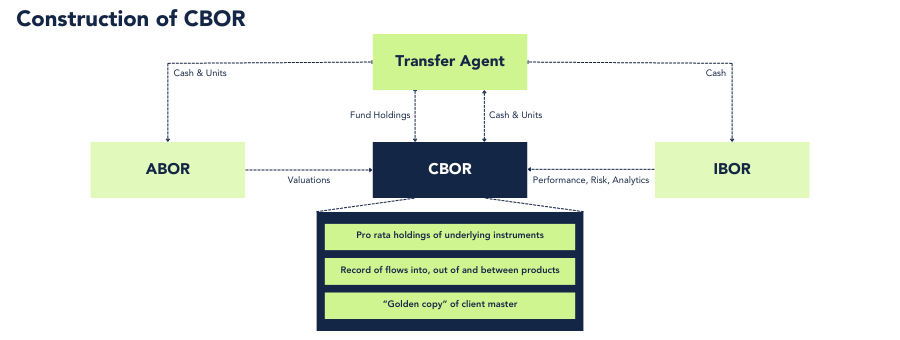

The introduction of the Client Book of Record (CBOR) places the client at the heart of the operation. Defined as the ultimate client “look through,” a CBOR goes beyond internal structures, showing client in- and outflows and providing insight into fractions of the underlying assets implied by the unit holding in any retail or commingled products. This shift directly addresses the limitations of existing platforms, including the Investment Book of Record (IBOR) and the Accounting Book of Record (ABOR), establishing a client-centric approach to investment management.

Front-office platforms (i.e., the IBOR) uphold the investment viewpoint originating from the manager’s internal structure, while accounting systems represented by the ABOR focus on the legal and administrative record. Introducing a client book of record (CBOR) alongside the IBOR and ABOR places the client as central to the operation, acknowledging their broader, long-term outlooks. These include considerations like allocation among various asset classes and managing relationships with multiple asset managers.

The Essential Steps to Building a Client Book of Record

The establishment of a bona fide CBOR demands a sophisticated data approach, enabling investment managers to shift from internal-centric methodologies to prioritising client perspectives.

From a data perspective, the crucial steps involve the set-up and persistence of a client account derived from a centralised portfolio master data set to support CBOR. Building a CBOR around a comprehensive client master, complete with reference data, KYC information and CRM details, becomes pivotal in enhancing business intelligence.

Further, the combination of client and portfolio classifications create a powerful tool for business development. Analysts can leverage the CBOR to discern the effectiveness of strategies across different segments. This holds particular significance to Sales and Marketing departments, as clients can be classified on broad “macro” attributes such as retail, wealth or institutional, as well as more specialised attributes related to demographics, time horizon, geography, and investment objectives. This comprehensive classification system empowers analysts to make informed decisions and adds depth to strategic business development initiatives.

The journey to a bona fide CBOR requires significant investment, as well as a vision that persists from where other core technology is lacking in client-centric data and intelligence. But while purpose-built platforms for CBOR remain rare, the current competitive landscape underscores the importance of showing clients that their investment possibilities and objectives are integral to the very foundation of the investment process. The transparency offered by a CBOR may take some getting used to, the investment manager’s ability to deliver on client requirements and anticipate them as they evolve will be essential to the manager’s survival and success.

Transformative CBOR Applications in Investment Management

By implementing Client Books of Record, investment managers can revolutionise their view on multi-asset allocation, achieve greater transparency across investment strategies and seek improved organisational collaboration. The following examples are just a sample of how CBORs can empower managers to elevate their operation.

1. Reimagining Organisational Structures: The role of CBOR in fostering collaboration

The importance of asset allocation, relative to selection, in generating excess investment returns is part of industry consensus, with much of the debate focused on the degree to which this is the case. However, for an industry that came of age in the heady days of the late-90s dotcom boom, managers have often designed their organisations around equity desks—parsing the instrument class into regions, sectors, and capitalisation ranges.

Though bottom-up selection remains an industry standard, the basis-points eked out each month by individual managers and analysts is of far more interest to the investment manager than it is to the client, who remains largely indifferent to the manager’s internal culture. Most important to the client are manager value added in aggregate, demonstrating awareness of:

- macro conditions,

- the client’s investment objectives,

- and flexibility in customising the instrument mix.

Whereas retail clients are often issued static snapshots of valued holdings, a CBOR treats client holdings as a dynamic portfolio, with a history and a track record that can be scrutinised more closely. This also allows for comparisons to market indices, benchmarks, and performance composites even for small retail investors.

2. Navigating Multi-Asset Allocation with CBOR Insight

The role of allocator-in-chief, especially for a multi-asset mandate, varies greatly by client. As discussed in our ESG whitepaper earlier last year, “personalisation,” or the ability to implement client-led investment directives, requires both technological advancement and a manager’s willingness to cede a high degree of discretion in investment decisions. This blurring of boundaries can make relationship management difficult but makes the client view provided by a CBOR more relevant.

Beyond this, a CBOR allows the manager to showcase its multi-asset capability, creating awareness of what is on offer, regardless of the original intent of the mandate. Analysis of CBOR activity can alert the manager to clients showing persistent negative performance, stagnant inflows, or routine outflows, creating an opportunity to target them with personalised marketing to keep them in the fold.

3. Strategic Transparency and Client Expectations: A CBOR revelation

.png?width=206&height=206&name=Blog_CBOR%20(2).png) It might be a shock to some to hear that a large investment manager has over 50 “unique” investment desks, leaving one to wonder whether their morning meetings were chaired by the CIO or Sisyphus, the tyrannical king whose eternal punishment was to roll a large stone up a hill, only to see it break away and roll back down once as he was about to reach the summit. When presented with a new investment platform with strategy-tagging capability, users are just as likely to relish in using it as they are to concern themselves with how easily and often new strategies can be added, "old” ones deleted and whether tagging a trade with a strategy is mandatory.

It might be a shock to some to hear that a large investment manager has over 50 “unique” investment desks, leaving one to wonder whether their morning meetings were chaired by the CIO or Sisyphus, the tyrannical king whose eternal punishment was to roll a large stone up a hill, only to see it break away and roll back down once as he was about to reach the summit. When presented with a new investment platform with strategy-tagging capability, users are just as likely to relish in using it as they are to concern themselves with how easily and often new strategies can be added, "old” ones deleted and whether tagging a trade with a strategy is mandatory.

From a client’s perspective, the notion that strategies are numerous, ever-changing, and an optional component of the investment process may be unsettling. This is where the CBOR steps in, putting the onus on the manager to demonstrate each strategy as a distinct value-add. “Look-through” client holdings at instrument level may also show that a client’s attempts to diversify their portfolio have resulted in highly correlated products with heavy concentration in the same assets.

Client Books of Record have the potential to bring a revolutionary force in reshaping investment practices. By placing the client at the core of operations, the CBOR transcends the limitations of internal structures (as well as the functionalities of ABOR and IBOR), and reveals client-centric insights, optimised to the client’s long-term perspectives. This client-focused approach addresses the shortcomings of existing platforms and fosters transparency, which allows investment managers to navigate multi-asset allocation, and meet client expectations to a greater extent. The establishment of a bona fide CBOR does require a sophisticated data approach, but the transformative impact on business intelligence and strategic decision-making underscores the vital role it could play in elevating managers’ offerings.

David Higgins

David oversees operations, strategy, and growth for Citisoft’s EMEA practice. He has worked with asset managers, service providers, software vendors, and regulators across the globe and has experience across the institutional, retail, wealth, and alternative sectors. David has extensive subject matter expertise throughout the investment management value-chain and has delivered recent strategic transformations for investment operations, fund accounting, transfer agency, custody, performance, data management, and reporting. David has lived and worked in the major financial centres of Europe, US, and Asia.

Comments